What Exactly Is a Stock Bubble?

A bubble is a kind of economic cycle characterized by a rapid increase in market value, notably in the price of assets. They are only noticed in retrospect after the bubble bursts. However, some experts have identified five phases of a bubble—a pattern to its growth and fall—that might help the unwary avoid being caught in its misleading clutches.

In an economic context, a “bubble” occurs when the price of a single stock, a financial asset, or even a whole sector, marketplace, or asset class—exceeds its significance by a wide margin. Since speculative demand, rather than fundamental value, drives inflated prices, the bubble ultimately but inevitably bursts, and enormous sell-offs force prices to fall, sometimes substantially.

The level of harm produced by a bubble bust depends on the economic sector(s) involved and whether involvement is broad or confined. For example, in Japan, the bursting of the equities and real estate bubbles in 1989–1992 resulted in a protracted period of stagnation for the Japanese economy — so long that the 1990s are known as the Lost Decade. In the United States, the dot-com bubble collapse in 2000 and the residential real estate bubble burst in 2008 both resulted in severe recessions.

How Does a Bubble Work?

Bubbles occur when the price of a thing increases beyond its true worth. They are often ascribed to a shift in investor behavior, although the exact reason is unknown. When there is a bubble in the stock market or the economy, resources are shifted to sectors of fast development. When a bubble bursts, prices fall.

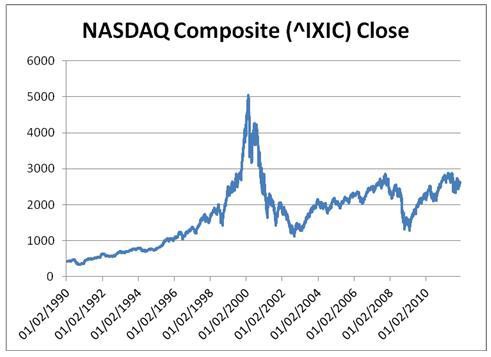

Following the partial deregulation of the country’s banks in the 1980s, the Japanese economy underwent a bubble, resulting in significant increases in real estate and stock values. The dot-com boom, often known as the dot-com bubble, was a late-90s stock market bubble. Excessive speculation in Internet-related enterprises defined it. During the boom, people bought technology stocks at high prices, assuming they could sell them at a more fantastic price until confidence was lost and a significant market correction occurred.

Examples of Bubbles

Recent history has seen two significant bubbles: the dot-com boom of the 1990s and the housing bubble of 2007 and 2008. However, the first known speculative bubble, which happened in Holland from 1634 to 1637, presents an instructive lesson for today. Some bubbles are more predictable than others. Traditional valuation measures in the stock market can be utilized to indicate excessive overvaluation. For example, a stock index trading at a price-to-earnings ratio double the historical average is certainly bubble territory. However, further study may be required to make a definitive decision. Other bubbles are more challenging to identify and may only be discovered retrospectively.

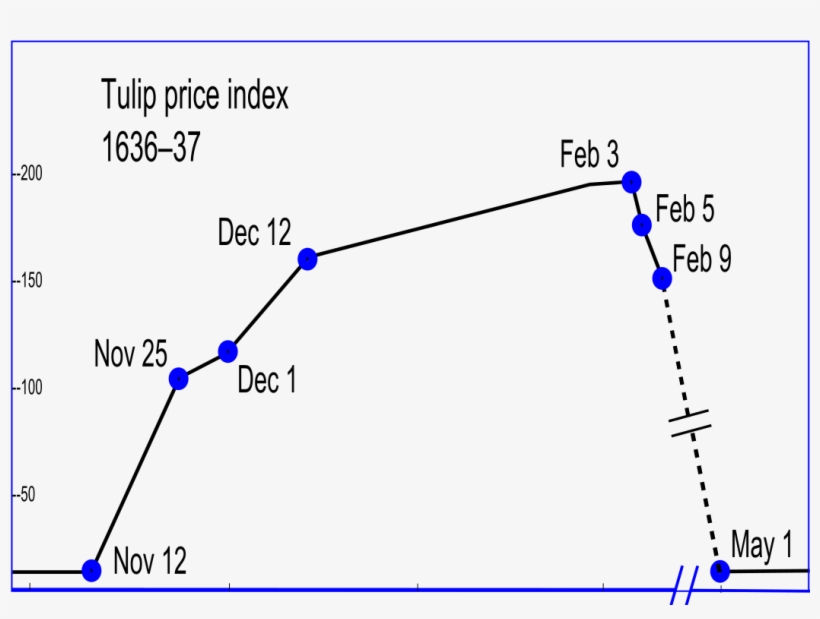

Tulip Mania

While it may seem ridiculous to assume that a flower could bring a country’s economy to its knees, which is precisely what occurred in Holland in the early 1600s. The tulip bulb trade began by chance at first. A botanist transported Tulip bulbs from Constantinople and planted them for scientific purposes. The bulbs were subsequently stolen and sold by neighbors. As a luxury item, the wealthy started to collect some rarer types. Bulb prices climbed as their demand increased. Some tulip cultivars demanded exorbitant prices. Bulbs were exchanged for anything having monetary worth, including houses and land. Tulip fever had caused such a frenzy at its apex that fortunes were made overnight. The establishment of a futures market, where tulips could be purchased and sold via contracts with no accurate delivery, encouraged speculation.

The bubble burst when a vendor planned a significant deal with a buyer who did not show up. Price rises were unsustainable at this stage. This sparked a panic that spread across Europe, reducing the value of each tulip bulb to a fraction of its previous value. The Dutch government intervened to calm the fear by enabling contract holders to release their obligations for 10% of the contract value: noblemen and ordinary alike lost riches in the end.

The Dot-Com Bubble

The dot-com bubble was defined by a spike in stock markets fueled by internet and tech enterprises investments. It arose due to speculative investment and excess venture cash flowing into young enterprises. In the 1990s, investors began pouring money into internet firms in the explicit belief that they would be lucrative.

As the technology evolved and the internet began to be commercialized, upstart businesses in the Internet and technology sectors helped drive the stock market’s 1995 spike. Cheap money and accessible capital fueled the next bubble. Many of these businesses barely made a profit or produced an actual product. Regardless, they could launch initial public offerings (IPOs). Their stock prices skyrocketed, causing a frenzy among eager investors.

Once the market peaked, investors panicked and dumped shares, causing a 10% drop in the stock market. Capital that was once easily obtained began to dwindle; enterprises with millions of dollars in market capitalization became worthless in a relatively short period. As 2001 came to a close, several publicly traded dot-com enterprises had gone bankrupt.

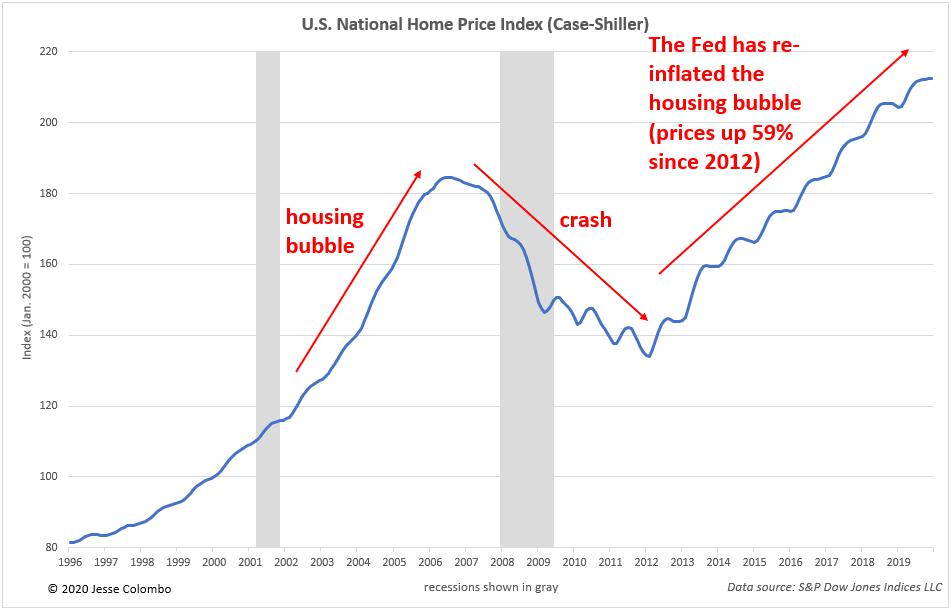

The US Housing Bubble

The housing bubble in the US was a real estate bubble that impacted more than half of the country in the mid-2000s. It was caused in part by the dot-com bubble. As the markets began to collapse, real estate prices began to increase. Simultaneously, the desire for homeownership began to rise to nearly frightening levels. Interest rates began falling. A concomitant driver was lenders’ permissive policy, which meant that almost anybody could become a homeowner. Banks began to reduce their borrowing criteria and slash their interest rates. With low starting rates and refinancing opportunities within three to five years, adjustable-rate mortgages (ARMs) became popular. Many individuals began to purchase properties, and others flipped them for a profit. However, when the stock market began to recover, interest rates began to climb as well. Mortgages for homeowners with ARMs began to refinance at higher rates. The value of these properties plummeted, triggering a sell-off in mortgage-backed securities (MBSs). This finally led to a situation in which mortgage defaults totaled millions of dollars.

In conclusion

Although each bubble is unique, most bubbles have in common the ability of members to suspend disbelief and overlook the growing number of warning indicators. Another factor is that the larger the bubble, the more harm it does when it explodes. Perhaps most importantly, the five most enormous historical bubbles and others along the road carry essential lessons for all investors.